3.4.1Climate Change Impact, Risk and Opportunity

OUR APPROACH

Climate change risks and opportunities are identified and assessed against SBM Offshore’s strategy in the risk breakdown structure. When relevant, these risks are included in the detailed review and analysis carried out for all tenders, projects and FPSO (asset) fleet operations that are part of SBM Offshore’s portfolio. The Risk and Control Manager facilitates the process and report to the Risk Assurance Committee (RAC) for consolidation purposes.

The outcome of the review by the RAC results in heat-maps of risks, which are presented in a quarterly risk report. This covers proposals, projects and fleets risks, as well as Group Functions and Execution Centers, and includes actions and managing measures in place to mitigate the risks. The report provides an overview to the Management Board and Supervisory Board alongside the measurement of SBM Offshore’s Risk Appetite Statements and the latest risk profile.

Between 2019 and 2021, SBM Offshore ran workshops with business, risk management and sustainability experts to identify climate risks for its business, segmenting between operations, offices and yards, following the TCFD frameworks. In the years following, SBM Offshore expanded its financial impact analysis and disclosures, which have been updated during 2023. During 2024, SBM Offshore continued to use the TCFD framework and adopted further physical climate-related hazards from ESRS 2 (IRO-1).

The outcome of this assessment is used to future-proof the current strategy against physical and transitional climate change-related risks and opportunities. Identified risks and opportunities are embedded in SBM Offshore’s risk-management approach. Based on the 2024 assessment, SBM Offshore has identified no significant financial impact, despite that cannot yet quantify the exact financial amount related to physical risks, transition risks, and potential benefits. According to the scenario analysis, SBM Offshore's current business model and strategy remain strongly resilient and there are no significant financial impacts on the consolidated financial statements resulting from climate risks anticipated under the different climate scenarios. See more information on the financial climate-related impact analysis in the financial statements, section 4.3.27.

Scenario Planning

SBM Offshore assesses potential material, physical and transitional climate change risks and opportunities as part of the risk management approach explained above. Integrated into this assessment is a resilience analysis for SBM Offshore’s activities in yards (upstream value chain), offices (own operations), and offshore assets (own operations). A full list of these assets and their locations can be found in section 1.2.1.

The used time-horizons of short-term, mid-term and long-term (current year, up to 2030, and beyond 2030), were selected to best reflect the lifetime of SBM Offshore’s assets and sites of operation.

SBM Offshore additionally looks at multiple climate-change scenarios to assess its risk and transition path. The scenarios are based on the International Energy Agency (IEA) and the Intergovernmental Panel on Climate Change (IPCC) data. In order to consider material physical and transitional risks, the below scenarios were deemed relevant:

- The RCP 8.5 scenario, a climate change scenario where climate mitigation actions are not taken and emissions continue to grow according to previous rates, i.e., a worst-case scenario.

- The RCP 2.6 scenario, a climate action scenario providing for strong commitment towards targets, as per the Paris Agreement, i.e., the scenario consistent with a 1.5 degrees scenario.

These two scenarios were selected to understand and plan for the highest level of possible risk from material transitional and physical risks. RCP 8.5 captures the worst possible future climate conditions and thus the best look at upcoming physical risks. RCP 2.6, on the other hand, captures the best possible future climate conditions but the highest transition requirements. This scenario will lead to the highest possible transitional risks for SBM Offshore.

Physical climate Risks

SBM Offshore recognizes that the physical climate risk assessment performed has limitations and assumptions attached. The assessment currently accounts for 28 climate hazards in accordance with ESRS E1. There are some additional hazards such as wind directionality, wave height and currents, all of which could pose future risks, especially to offshore assets. These hazards were left out of scope due to a lack of sufficient data, but it is planned to include them in future assessments. The assessment also has a limited inclusion of SBM Offshore’s supply chain, only assessing key upstream suppliers (yards), as disruption of these suppliers would cause the greatest risk.

For the physical climate risk assessment, all 28 of the climate hazards suggested in ESRS E1 were considered. 12 hazards were deemed material for onshore assets and 12 were deemed material for offshore assets, covering 19 of the 28 hazards. 13 of these were assessed using each asset’s geospatial coordinates and the IPCC’s CMIP6 database to obtain environmental conditions for all assets, in all three time-horizons, for both climate scenarios.

The remaining six hazards could not be assessed through the CMIP6 database and were instead assessed using available online tools and the results of academic studies. The results for these hazards also relied on the geospatial coordinates of each asset but it could not always achieve separate results for each time-horizon and climate scenario, with some relying on the current risk of hazards. Despite being deemed material, coastal erosion could not be assessed due to a lack of reliable data either in the CMIP6 database or in available online tools.

Offshore

Of the 12 material hazards, four hazards were determined to pose some level of risk to offshore assets, including ocean acidification, saline intrusion, heat stress and cyclones. It was also determined that changes in wind patterns might pose a risk, but further investigation is necessary before a conclusion is possible regarding this hazard.

Both ocean acidification and saline intrusion (assessed as saline levels in seawater) have the potential to accelerate the corrosion process of submerged metal, such as hull and mooring systems. If accelerated enough, corroded metal would either need to be replaced or could shorten the expected operational lifetime of offshore assets. However, the current study was not able to identify the likelihood of this risk, only the possibility of the risk. Additional investigation into the identified future climate conditions is necessary to determine if this is a realistic or overly cautious risk.

The possibility of cyclones is an ongoing risk for offshore assets in areas where cyclones could happen. Future conditions within SBM Offshore’s time-horizons are only expected to marginally affect the intensity of cyclones. As such, offshore assets are not expected to face an increased level of risk, only the ongoing possibility of damage from cyclones.

Heat stress is the hazard identified with the largest levels of change. Heat stress can affect workers on offshore assets, potentially preventing necessary work outside of controlled conditions (where air conditioning is not possible). This is especially true for offshore assets in Angola, Equatorial Guinea, Malaysia and the United States, where the greatest level of change is expected. Work is currently being done on protective equipment that could mitigate the risk from heat stress.

Physical Risks Hazards Parameters

Classification of climate-related hazards (Source: Commission delegated regulation (EU) 2021/2139) | |||||

|---|---|---|---|---|---|

Temperature-related | Wind-related | Water-related | Solid mass-related | ||

Onshore Assets (Office, R&D Laboratory, Yards, and shorebases | Chronic |

|

|

| |

Acute |

|

|

| ||

Offshore Assets (FPSOs) | Chronic |

|

|

| Not applicable |

Acute |

|

|

| ||

Onshore

For onshore assets, it was determined that seven hazards would pose a risk. This includes heat stress, water stress, floods (river and coastal), landslides, wildfires and avalanches.

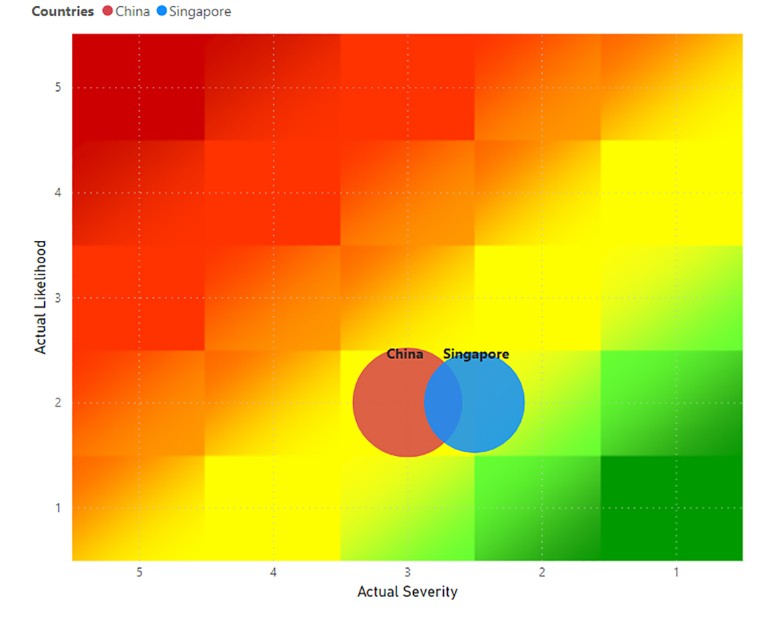

Heat stress is primarily expected to affect construction yards, as work in offices, shorebases and R&D labs occur in environments with ready access to air conditioning. Of the yards utilized by SBM Offshore, the yards in China and Singapore are expected to be affected at some level. If conditions become dangerous, heat stress might result in necessary shutdowns, delaying construction projects.

Water stress was assessed using available online tools, and the degree to which local infrastructure is likely to be affected is unknown. With the results available, water stress affects the majority of onshore assets, with the exception of those in the Netherlands, Brazil, Switzerland, Equatorial Guinea, the United States and Singapore. Typically, onshore assets have ready access to water, but additional water sources or ready access might need to be identified if conditions progress according to the risk levels projected.

Heat Stress Analysis (Onshore location examples)

Both the effects of river and coastal flooding were assessed for onshore assets, including the influence from sea level rise. As with water stress, it is unsure to what extent the available tools consider local defenses against river and coastal flooding. Half of the onshore assets in China, a few in Brazil, and one each in Angola and Guyana are at risk from the effects of flooding, according to the current predictions. Flooding could cause direct damage to assets or people, or otherwise result in shutdowns and maintenance, delaying construction projects and necessary onshore support to offshore assets.

Landslides, wildfires and avalanches have the highest level of uncertainty in their results. Available tools assess risk by determining if conditions will allow for the occurrence of these hazards. For example, if an area might be conducive to a wildfire, it will be marked as at risk, regardless of proximity to forest cover. In total, five assets were determined to be at risk from these three hazards. If they occur, these three hazards could cause physical damage to assets or people and could delay construction projects. In the future, additional investigation will be performed to lower the level of uncertainty and determine the likelihood of the risk from these hazards.

Climate scenario RCP 8.5

Risk | Asset type | Operational impact | Financial impact | Management of impact |

|---|---|---|---|---|

Ocean acidification | Offshore | Accelerated corrosion of submerged metal, such as the hull and mooring systems. If accelerated enough, corroded metal would either need to be replaced or could shorten the expected operational lifetime of offshore assets | Increased cost of construction and repair costs for damage, insurance, contingency | Design specifications of units take into account the latest metocean simulations of extreme weather events. |

Saline intrusion | Offshore | |||

Cyclones | Offshore | Physical damage to infrastructure | Increased cost of construction and repair costs for damage, insurance, contingency | SBM Offshore mitigates risks from climate change impact to people and the environment for specific scenarios in each location. For example, the preparation and execution of Health and Safety plans during the execution of SBM Offshore’s projects and readily available Emergency Response plans. Associated financial impacts are mitigated in contingencies for additional schedule impacts, adequate safety measurements and cover through insurance. |

Heat stress | Offshore/ Onshore | Increased work strain for construction and offshore workers − decreased productivity and delays | Increased cost of construction | |

Water stress | Onshore | Increased delays in steel production due to water scarcity Unhealthy work conditions | Increased cost of construction, water expense Higher cost of safe water supply to people | |

Flooding | Onshore | Physical damage to infrastructure or harm to people, resulting in shutdowns and maintenance, delaying construction projects and necessary onshore support to offshore assets | Increased cost of construction and repair costs for damage, insurance, contingency | |

Landslides | Onshore | Physical damage to assets and potential harm to workers | ||

Wildfire | Onshore | |||

Avalanche | Onshore | |||

Transition climate Risks

As the world faces increasing difficulty in aligning with the IEA’s Net Zero Emissions (NZE) scenario, the path to limiting global warming to 1.5 degrees has become more challenging. Although renewable energy expansion remains critical, market headwinds – including robust global demand for hydrocarbons and barriers to renewable project scalability – complicate this transition. Without enhanced mitigation measures, the UN projects that warming could highly likely exceed 2.5 degrees over the course of this century, posing substantial implications for energy companies navigating the shift to a low-carbon economy.

Financing Landscape Shifts

One notable transition risk is the evolving financing landscape, particularly in Europe, where Export Credit Agencies (ECAs) are reducing their support for oil and gas projects. This shift may elevate the cost of capital for energy projects, creating new financial pressures on the industry. To address this, SBM Offshore is actively engaging with clients on alternative commercial models to adapt to these changes and is in dialogue with potential lenders to assess their support for future projects under varying climate scenarios.

Product Development Delays in New Energies

Another transition risk lies in the potential for delays in new energy project development, particularly offshore wind. Inflationary pressures and a shifting subsidy landscape have impacted certain industry players, underscoring the risk of financial setbacks and slowing momentum for renewable investments. In response, SBM Offshore has adopted a selective strategy for its New Energies portfolio, prioritizing offshore wind projects that are both viable and capable of achieving the scale necessary to drive renewable energy affordability.

Further data on transition climate risk analysis is provided in the table below. SBM Offshore’s scenario analysis continue as an iterative process to critically assess and prepare for evolving climate and market conditions, serving as a tool to explore potential transition pathways rather than predict specific outcomes.

Climate scenario RCP 2.6

Risks | Operational impact | Financial Impact | Management of Impact |

|---|---|---|---|

Inability to attract employee/resources | Decreased development in renewable product market, FPSO projects understaffed, net zero targets at risk | Increased cost due to use of contractors rather than attracting in-house talent, potential cost of non-quality | SBM Offshore remains focused on being an attractive employer, with interesting opportunities in the energy industry. Moreover, SBM Offshore applies its unique capabilities to unlock new markets for energy transition. |

Clients not supporting low-emission effort | Reduced direct income from net zero aligned technologies, net zero targets at risk | Potential increased cost for SBM Offshore when clients are not committed to low emission efforts. | Early engagement with clients on net zero paths, whilst continuing to develop emissionZERO® and achieve SBM Offshore’s net zero targets. Leverage on SBM Offshore collaboration to accelerate energy transition. |

Reduced demand for oil and gas leads to clients terminating contracts | Reduced operational activities for traditional FPSOs | Decline in future revenues and earlier than expected decommissioning costs, managed through contract termination compensation | SBM Offshore has a compensation structure for contract termination and decommissioning costs. SBM Offshore continuously updates its offer in light of the changing energy landscape and aims to decarbonize its existing and new units through emissionZERO®. |

Financing constraint for hydrocarbon-related projects | Alternative financing arrangements | Increased cost of financing, potential change in economic distributions, lower margins | Adequate access to debt and equity funding is secured through use of SBM Offshore’s existing liquidity, by selling equity to third parties, the use of bridging loans and long-term project financing. Debt funding is sourced from multiple markets, such as international project finance banks, capital markets transactions and Export Credit Agencies. Enlargement with providers of alternative financing. |

More stringent social and environmental laws | Increased liabilities or provisions, and assessments of contingent liabilities | Increased cost of production, limits to field development | The close monitoring of laws and regulations is carried out continuously, and substantive changes are escalated. This includes liability from an emergence of carbon tax and its mitigation through appropriate clauses in contracts. |

Introduction of carbon pricing | Decrease in total primary fuel consumption and total energy input | Increased environmental tax and carbon pricing | |

Delay in product development | Deviation from company net zero path | Decreased potential for revenues from renewables associated with 2030 ambitions | SBM Offshore focuses its project development efforts to achieve greater progress, both in core operations and in new markets, by expanding its interests within the energy industry and its horizons into other sectors. |

According to the United Nations’ world population projection, by 2050, world population will surpass 9.7 billion people, with around 68% of the total population living in big cities close to the oceans. Global energy demand is set to grow in the coming decades. While oil and natural gas will still play a key role in the primary energy mix, renewable energy is increasing its share and governments are raising their decarbonization targets. The demand for new oil and natural gas projects is expected to continue to grow until the end of the decade, as geopolitical tensions have underlined fragilities and dependencies in the energy system, after which it should slightly decline until 2050. Geopolitical events make energy supply and demand inherently volatile.

SBM Offshore expects that, in the coming years, there will be a need for its capabilities to deliver sizeable deepwater projects across the energy mix. GHG emissions for deep water are comparatively lower than other oil supply projects. As such deepwater oil should be part of the energy transition set of solutions.

SBM Offshore’s success will depend on partnering with other companies similarly committed to its energy transition strategy and activities, with a focus on the lifecycle value of projects, from early client engagement to the end of field recycling phases.